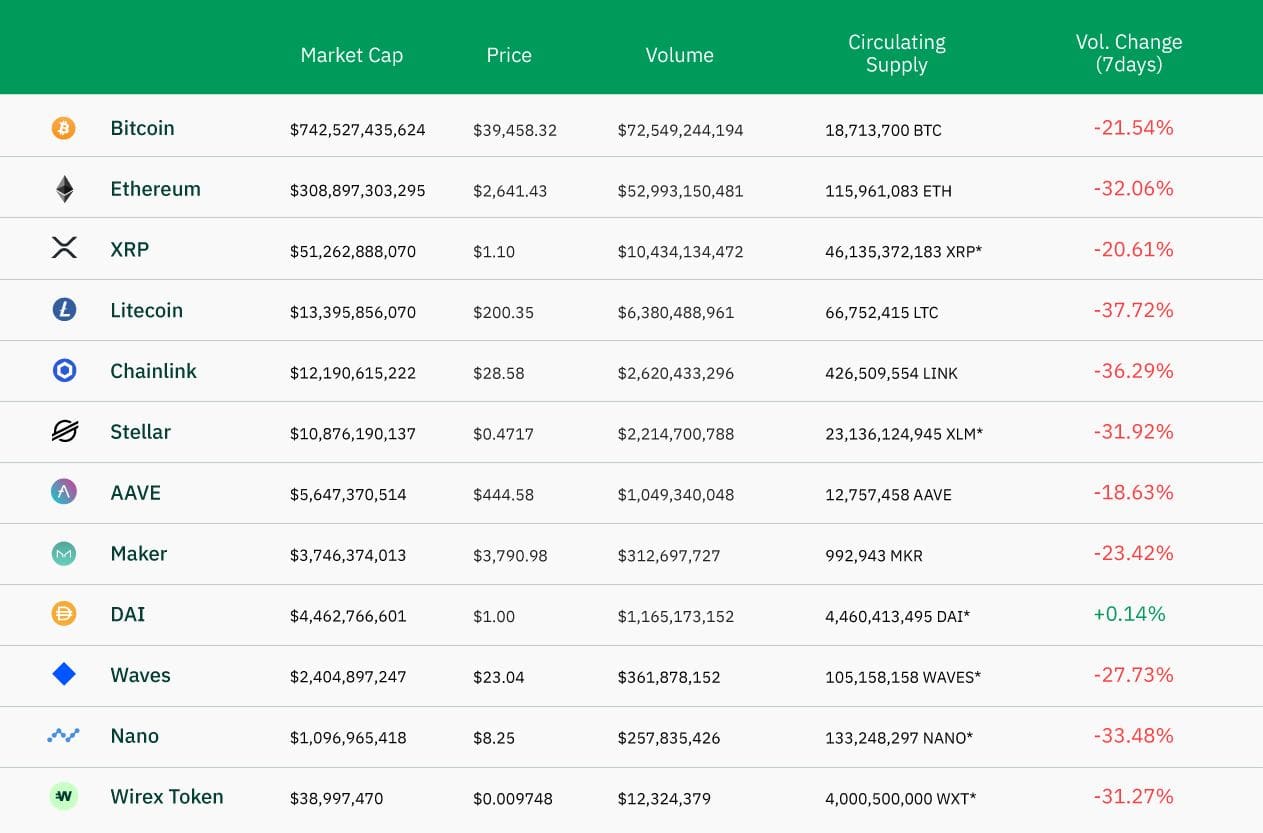

data taken at 9:46 am 21/05/2021

Panic swept the cryptocurrency markets this week as the Bitcoin price tumbled below $40,000, printing its lowest level since the end of January at $30,066 (source: Bitstamp). The plunge initially followed the suspension by Tesla of its vehicle purchases with Bitcoin. The suspension fuelled speculations over the status of the estimated 38,300 Bitcoins held on its balance sheet as of last month. Elon Musk’s clarification that ‘Tesla has not sold any Bitcoin’ did little to avoid the worst correction since March 2020.

The IRS and Justice department’s investigation of Binance, the first cryptocurrency exchange, as well as China’s announcement of a cryptocurrency business ban for financial and payment institutions this week exacerbated the downturn. The Bitcoin price dropped by nearly 53.8% from its all-time-high recorded on April 14th. The amplitude is still below the 63.62% correction of March 2020, but more severe than any of the corrections experienced during the last extraordinary rally in 2017 (down 40.29% in June-July 2017). In this context, it is difficult to defend the idea that the involvement of institutions could improve the market’s resiliency in the short term. Tesla was once hailed as the forerunner for large institutions in the adoption of cryptocurrencies. It is now potentially one of the biggest disappointments for the sector. The market is expecting the carmaker to get rid of its BTCs, five months only after announcing their purchase.

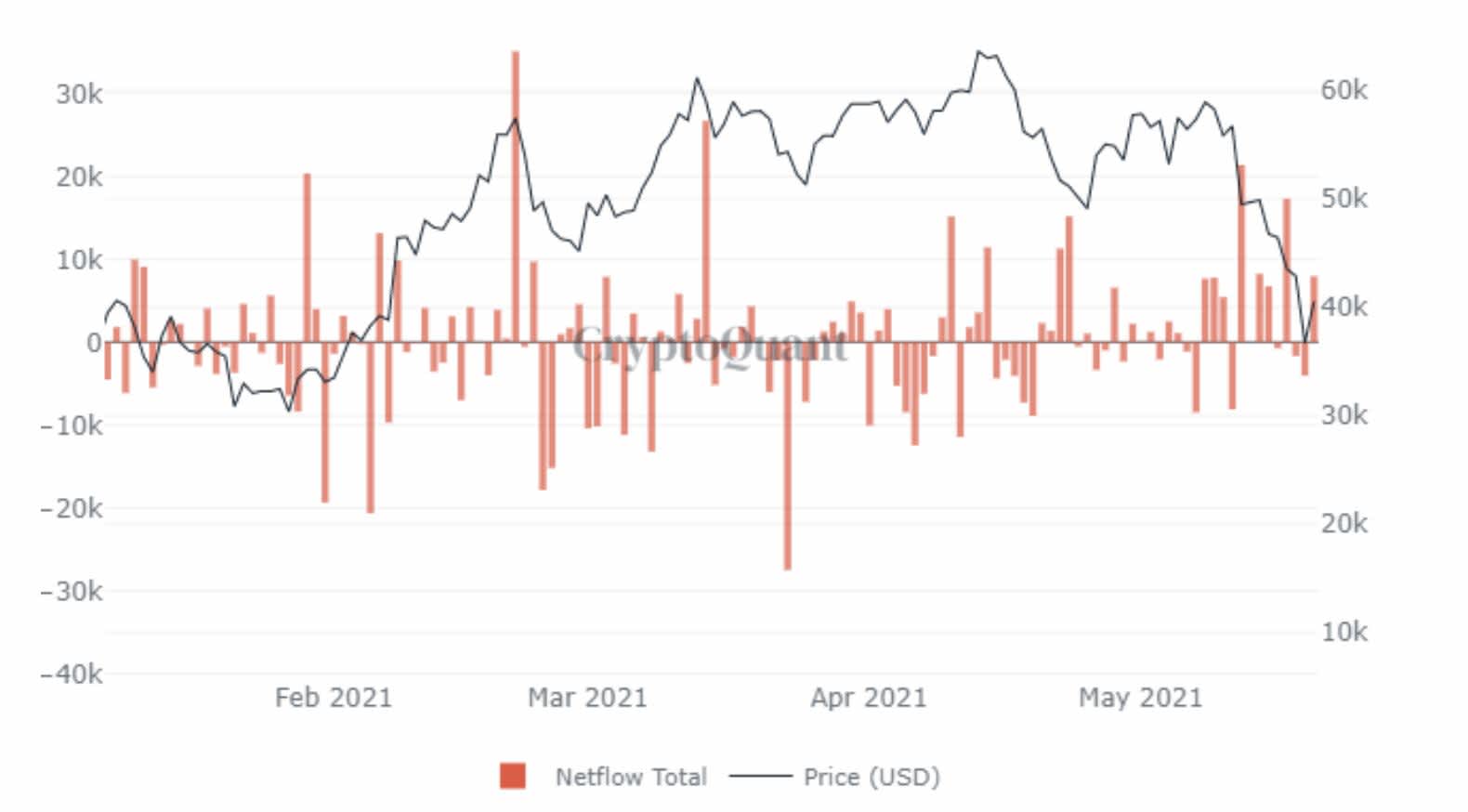

The Bitcoin all-exchanges netflow recorded negative figures on May 18th and May 19th, but again another positive jump yesterday of 7,937 BTCs, the 8th positive jump above 5,000 BTCs this month, suggesting that the rebound would not be a matter of days. The post-March 2020 recovery lasted three months. Likewise, it could take weeks for investors to regain confidence.

Cryptoquant’s ‘BTC All Exchanges Netflow : the difference between BTC flowing into and out of all exchanges’ shows a large concentration of positive daily figures this month.

$7.56 billion of long BTC future contracts were liquidated on May 18th according to bybt. It is the highest daily figure since March 2020. These forced liquidations, that are essentially automatic market sell orders sent at the worst of the market correction, pave the way for rare buying opportunities: the market bounced back fast to $40,000. The growth of BTCs held in derivative exchanges’ wallets accelerated since the beginning of April. More BTCs were also sent during the correction. The inflow of BTCs to derivative exchanges, in the middle of a panic sale, typically happens to top up the collateral value and avoid a forced liquidation. New BTCs are also collateralised to re-build a long futures position that would have been liquidated, and therefore seek profits from a potential price recovery. But it is not always that easy…

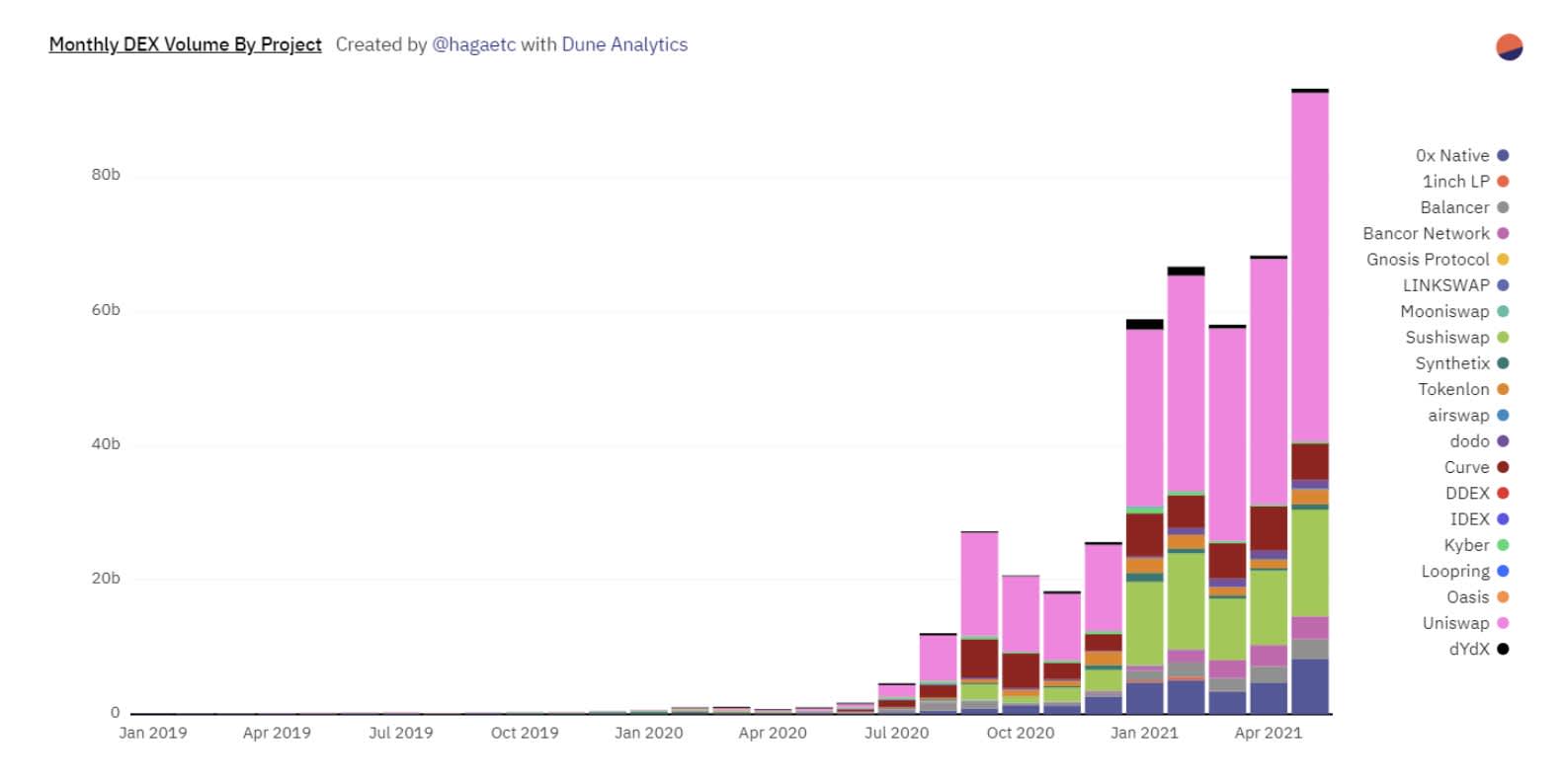

In fact, it is hard to trust that any online exchange would operate ‘normally’ during a severe market correction. Binance, Coinbase, Gemini and many others experienced serious disruptions over the exceptional load of online connections and requests, causing further anxiety among small investors. The consequent lack of liquidity certainly precipitated the BTC/USD fall by thousands of dollars. At the same time, trading volumes of on-chain decentralised exchanges (DEX) soared. This month is by far the best on record for DEXes, with defiprime reporting close to $90 billion exchanged so far.

This is a strong win for the cryptocurrency markets. It is an undeniable show of strength by the on-chain economy. DeFi platforms are now well established and more reliable than ever, offering more investment opportunities. They are almost ready to take over the centralised exchanges. The release this month of Uniswap’s v3 protocol is another step forward that introduced more flexibility for the market-maker. It is one essential step towards a fully-fledged on-chain decentralised exchange that would easily compete with any centralised exchange.