data taken at 9:51 am 26/03/2021

The Bitcoin price dropped by nearly 10% this week, extending a correction that started on March 14th. The first cryptocurrency conceded more than 15% of its value from the all-time-high reached on March 13th. The correction is mostly due to the large expiration of future and option contracts this morning. And this is most likely due to ‘carry trades’.

First of all, let’s go over the characteristics of a ‘carry trade’ strategy:

A ‘carry trade’ strategy is a classic strategy used to profit from the difference between the price of an asset (e.g. BTC/USD) and the price of its future contract (e.g. BTCM2021: the June BTC future contract). The difference (also called the ‘basis’) between the June future contract and the Bitcoin price exceeded an equivalent annualised rate of 20% at many occasions this year. A wide basis would motivate carry traders to sell Bitcoin futures and buy Bitcoins (cash) against them. The combined exposure of the futures and Bitcoins should be close to zero (also called ‘flat exposure’). If a carry trader holds her position until the expiration of the futures, she would have locked the difference as profit, because by definition, the future price always converges towards the Bitcoin price at expiration.

The March, April, and June basis collapsed two days ago. Only the December basis was moving yesterday in the opposite direction. It is quite usual to see the basis expand when the Bitcoin price goes up, and contract when the Bitcoin price goes down. The expansion is an indication of increased leverage in the market, and the contraction is an indication of de-leveraging.

When we get close to the expiration date, carry traders can choose either to:

- let their futures expire, and sell the Bitcoins they hold against them

- or ‘roll’ their positions to the next maturity. A ‘roll’ consists of buying back the March futures, selling the Jun futures, and of course keeping the Bitcoins.

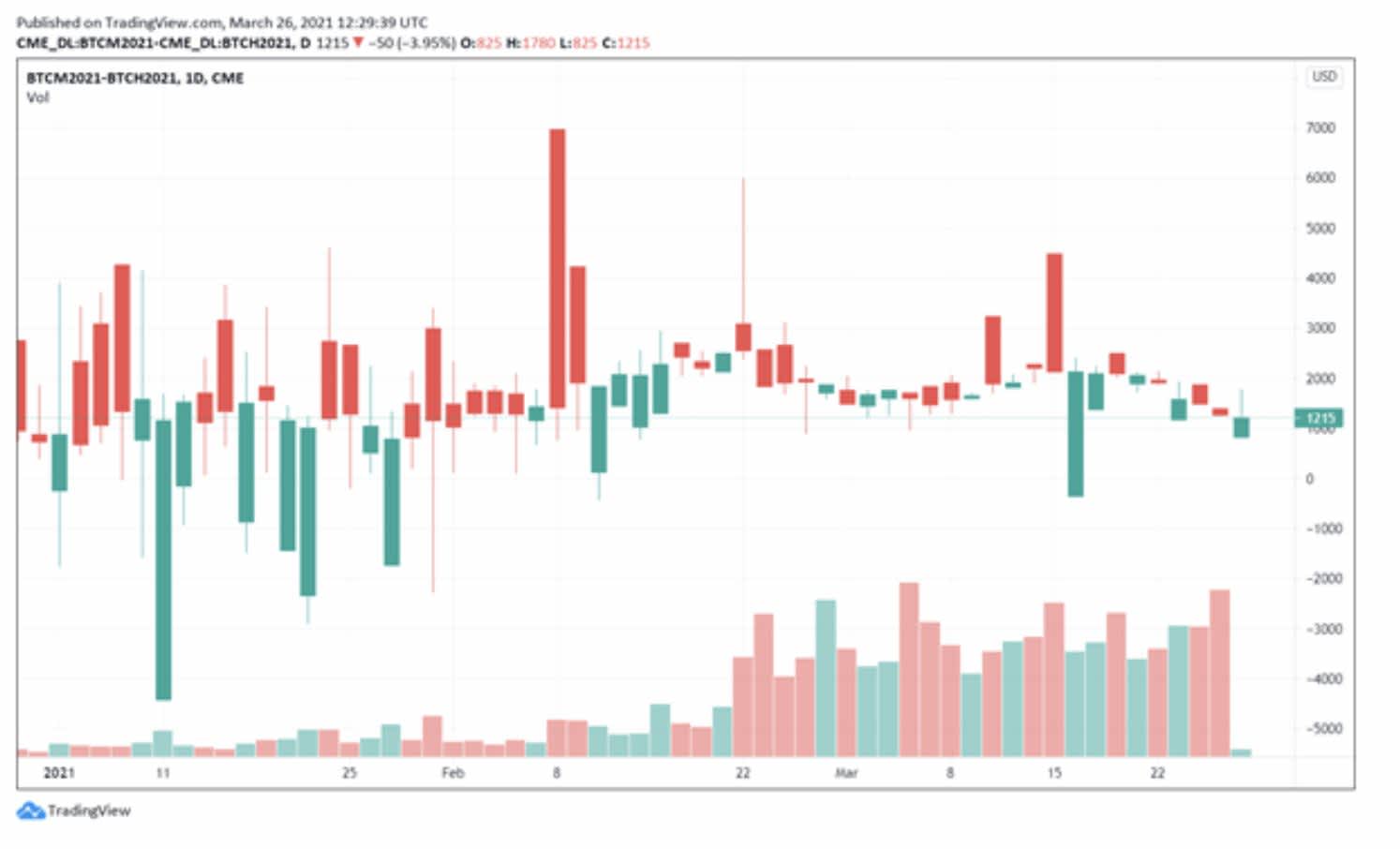

Selling the June future contract and buying the March future contract is equivalent to selling the ‘roll’. And this is what happened during the past few days: carry traders sold the ‘roll’, and the value of the ‘roll’ dropped from $2,500 to $1,000.

Source TradingView.

The Roll: the difference between the CME June future contract (BTCM2021) and the CME March future contract (BTCH2021). traders have been selling more of the june future contract.

But this doesn’t explain yet why the Bitcoin price lost 10%.

In fact, if the April, May and June basis collapse, there is little interest for carry traders to roll their positions because the expected profit from locking the basis spread would be consequently small. In this case, carry traders would let their March futures expire, and the Bitcoins they hold against these March futures would be sold, driving the Bitcoin price further down. This is what most likely contributed to the Bitcoin price correction.

There was nothing this week to support the Bitcoin price back to the 60,000 levels. There was nothing to resist the downward pressure exerted on the market: the futures open interest hit a record 22.9bil thirteen days ago according to the Block, and $6 billion worth of Bitcoin options expired today. As usual, the forced ‘long liquidations’ of leveraged positions that followed the first days of the market correction exacerbated the market’s losses.

The technical correction could be considered as an opportunity to buy. But Institutions are more cautious now. The Grayscale fund has been trading at a systematic discount since the end of February. The discount is now at -9.74%, even reaching a record at -14.34% two days ago. How long could Grayscale sustain this discount before it starts selling BTCs? We are here in unknown territory.

Looking at the metrics, the Ether (ETH) also seems to be under pressure this week on the institutions front. However the amount staked in the Beacon chain is growing slowly, and the amount of ETHs locked in DeFi reached today 9.347mil, a new all-time-high. The average Ethereum transaction fee is still high, above the $16 mark, driven by the Decentralised Finance sector (DeFi), but also by the craze around Non Fungible Tokens NFTs. When a growing 3% of the Ethereum total supply is staked and a growing 8.2% is locked in DeFi, the Ether might still have some interesting potential this year.