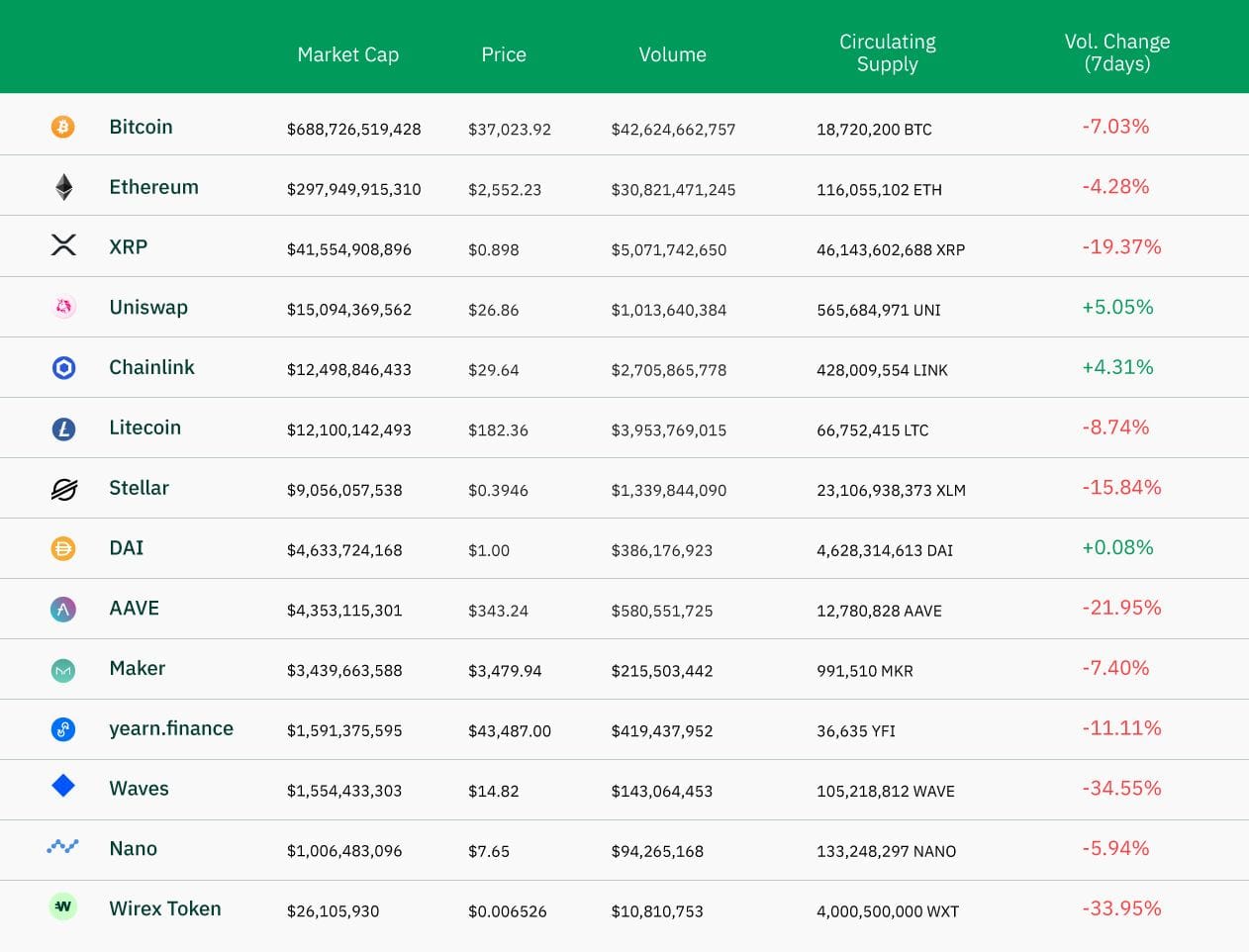

Data taken at 9:37am 28/05/2021 - Coinmarketcap

The Bitcoin (BTC) price is holding right below the $40,000 level, swinging now around the $36,000 and $37,000 price levels. As mentioned last week, the recovery is most likely a matter of weeks. Meanwhile, on-chain data suggests that the panic sale is behind us, as the total netflow of BTCs on exchanges is negative at -15,200 BTCs. In other words, 15,200 BTCs have been withdrawn from exchange wallets according to Cryptoquant. The flow of BTCs is nearly flat for Coinbase. With roughly two thirds of its trading volume coming from institutions, the Coinbase flow indicates that institutions are holding.

On the contrary, there is still a significant net inflow of BTCs on Binance this week: a net total of 6,000 BTCs were deposited in the retail-oriented leading exchange. The net flow reached a weekly peak on Sunday. Given the low market depth observed on weekends, prices are more prone to sharp downward movements. The weekend activity is also more retail-oriented, which confirms the sentiment that retailers are still stunned by the ferocity of last week’s correction, looking to sell at the next opportunity.

In this context, this week’s rebound was short-lived: from the low $31,100 on Sunday, to the high $40,900 on Wednesday, and then back below $36,000 at the time of writing. The rebound was mostly opportunistic, but it could also be attributed to Paypal’s announcement that it would let customers send the tokens they buy to the destination of their choice.

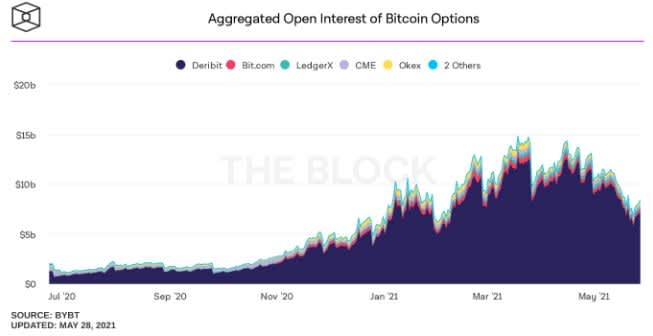

The market is still fragile, and speculators are still driving its ups and downs. Today’s expiration of BTC option contracts is the smallest this year after the recent drop forced most contracts into liquidation. It is still higher than any of the last year’s expirations.

Retail investors used leverage excessively. Hedge funds borrowed heavily. They used the multiplier effect to seek the highest possible exposure to the market, and the highest potential profit. Mark Cuban illustrates the multiplier effect in a tweet on Sunday:

“A trader borrows to buy ETH, uses ETH to borrow stablecoins, uses that to [provide liquidity] to a high APY pair (…)”.

If loans were over-collateralized, the multiplier effect would be limited. If a trader can borrow 60% of the collateral posted, post the borrowed amount to borrow once more, and repeat the process indefinitely, then the maximum value she can borrow is 150% of the collateral’s initial value.

Most crypto loans today are reasonably over-collateralized. But more projects do offer uncollateralized crypto loans: Centralized projects like Celsius, or Decentralized Autonomous Organizations (DAO) like TrueFi or Aave.

Lenders of unsecured loans like Celsius would argue that their borrowers are large institutions with an excellent credit grade. But the selection of borrowers is far from transparent, and the recovery of the loan amount would be at best protected by “law” as opposed to “value”. A project that promises high returns to a community on major cryptocurrencies could unreasonably seek higher returns elsewhere, regardless of the default risk. Protecting an unsecured loan by law does not improve the recovered amount if the borrower’s default is inevitable.

Even though it is possible to devise digital legal wrappers that are governed by traditional law, this would also go against the decentralization principle. From a decentralization perspective, the general message would be that holders are free to lend their tokens to anyone they deem reliable, on the terms of their choosing. The KYC and legal terms could be conducted on a peer-to-peer level.

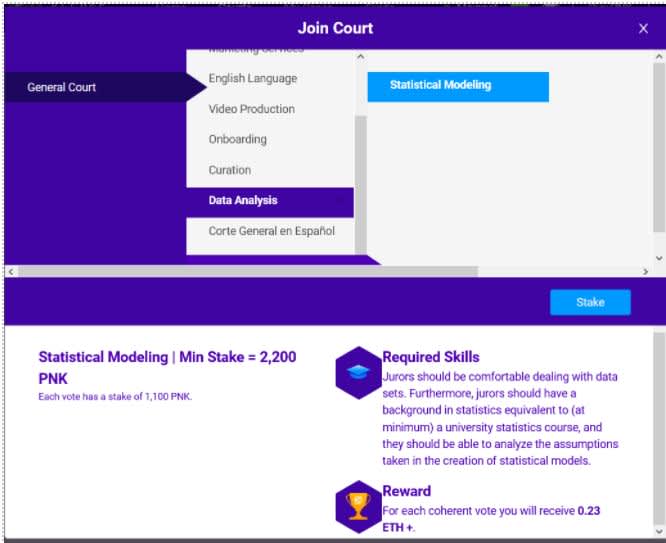

If the concept of smart legal contracts seems appealing at first, the practical steps to enforce these contracts are far from decentralized. As such, they are expensive and time-consuming. Instead, decentralized solutions are being designed. Kleros aims to decentralize the arbitration system, creating a community of jurors, and giving the parties to a dispute the option to get a fast and cheap decision. Anyone can join a court and contribute to the resolution of a dispute. There are 9 courts already available, and every court has its specialty: marketing, data analysis, onboarding. Kleros is used on DEXes like Uniswap for instance to vet the new tokens added to the protocol.

There are now 178,100 BTCs locked in DeFi projects according to defipulse. The level is growing closer to the February high at 194,500 BTCs. The DeFi economy is experimenting and expanding despite the short-term speculations.