data taken at 9:40 am 30/04/2021

Supported by strong fundamentals, the Bitcoin price (BTC/USD) eventually bounced back from this week’s low at $47,004, to the $56,500 level reached on Wednesday. But the SEC decision two days ago to delay once more the approval of a Bitcoin ETF did weigh on the market. It contributed to a 7.8% price correction from Wednesday’s high to Thursday’s low.

Indeed, the approval of the VanEck Bitcoin ETF was disappointedly delayed by another 45 days. Yet, the race for the first US Bitcoin ETF continues: The SEC announced the very next day that it would start to examine the proposed listing of another candidate: the Kryptoin Bitcoin ETF.

The SEC still considers that listing a Bitcoin ETF goes against the “requirement that a national securities exchange’s rules are designed to prevent fraudulent and manipulative acts and practices”. In other words, the SEC still supports that most of the Bitcoin volume traded on exchanges is still fake, and prone to manipulation. As a result of the delay, the hope to see a Bitcoin ETF launch revive the institutions’ interest in the first cryptocurrency has also been deferred.

The growth of the Grayscale (GBTC) holdings has remained flat since the end of January, and the holdings of the Canadian Bitcoin ETFs are also losing steam. The number of Bitcoins held by the Purpose Bitcoin ETF has increased by a small 6,300 Bitcoins since our last check 50 days ago.

The first cryptocurrency is back in the uncertainty zone between the $50,000 and $60,000 levels. The price correction from the all-time-high did not raise any panic among Bitcoin holders but some indicators might be showing some signs of short-term weakness. On the supply side:

- Cryptoquant’s ‘all exchange reserve’ and the ‘all exchanges net flow’ increased by a total 30,000 BTCs over the past 10 days, with a net 9,000 BTCs sent to exchange wallets only in the past 2 days.

- Miners also sent 5,000 BTCs to exchanges over the same period.

Against this total potential supply of 35,000 BTCs, there are:

- roughly 9,000 additional WBTCs that were locked in Defi projects over the last 10 days.

- and an extra 7,000 BTCs added to the Bitcoin ETFs.

The BTC supply and demand metrics are nowhere near the bullish metrics we observed on February 5th. Consequently, the Bitcoin dominance extended its losses this week, losing 2% more, and dropping to a level that was last seen in July 2018.

TradingView Bitcoin market cap dominance at 49.3%

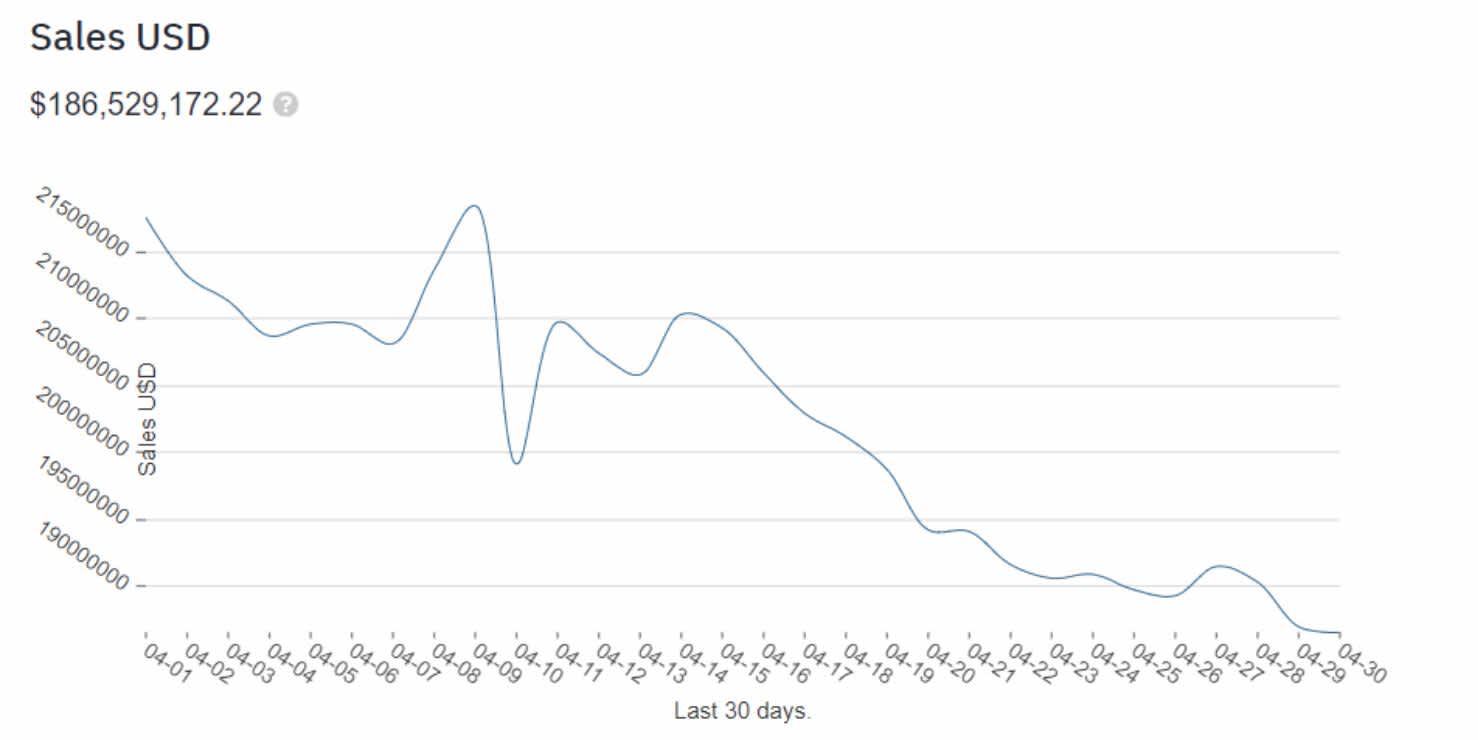

The first reason for the decrease of the BTC dominance is the outperformance of its eternal second: The Ether (ETH). The ETH/USD pair reached a new record high today at $2,802. Ethereum’s Non-Fungible Token (NFT) craze has probably come to an end as the total NFT sales in USD lost nearly 15% over the last 30 days. Still, in sharp contrast with Bitcoin, the Ethereum project unexpectedly benefits from a renewed interest.

Source: nonfungible.com

Global drop of the daily NFT sales (in USD) This time, the renewed interest came from the traditional financial sector. The European Investment Bank (EIB) announced three days ago its intent to issue digital bonds on the Ethereum blockchain for €100mil. According to