Cryptocurrency markets rebounded this week, recouping a fraction of the losses suffered after the ETFs approval by the SEC 20 days ago. The Bitcoin price in US dollars is up by 7.6%, now swinging around the 43,000 level. The Ether price (ETH/USD) is up 4.5%. The implied volatility dropped back to November levels last week, pointing towards a likely consolidation.

Also pointing towards consolidation: the fact that trading volumes are down on-chain and off-chain. Daily volumes on-chain halved compared to the best daily volumes observed 2 to 3 weeks ago. Looking at the month of Jan so far, we can also see that DEXs on Arbitrum and Solana are gaining market share, with Arbitrum in second place. Both protocols are performing well this week: ARB (+7%), SOL (+14%).

The large part of the rebound happened on Friday around the January expiration time of option contracts. We had the Deribit options expiring at 8am UTC that day, and CME options expiring at 15pm UTC. The market jumped by more than 5.6% from 8am that day.

Remember that we had a large amount of call options at the 50,000 dollars strike, so way above current prices, that eventually expired worthless.

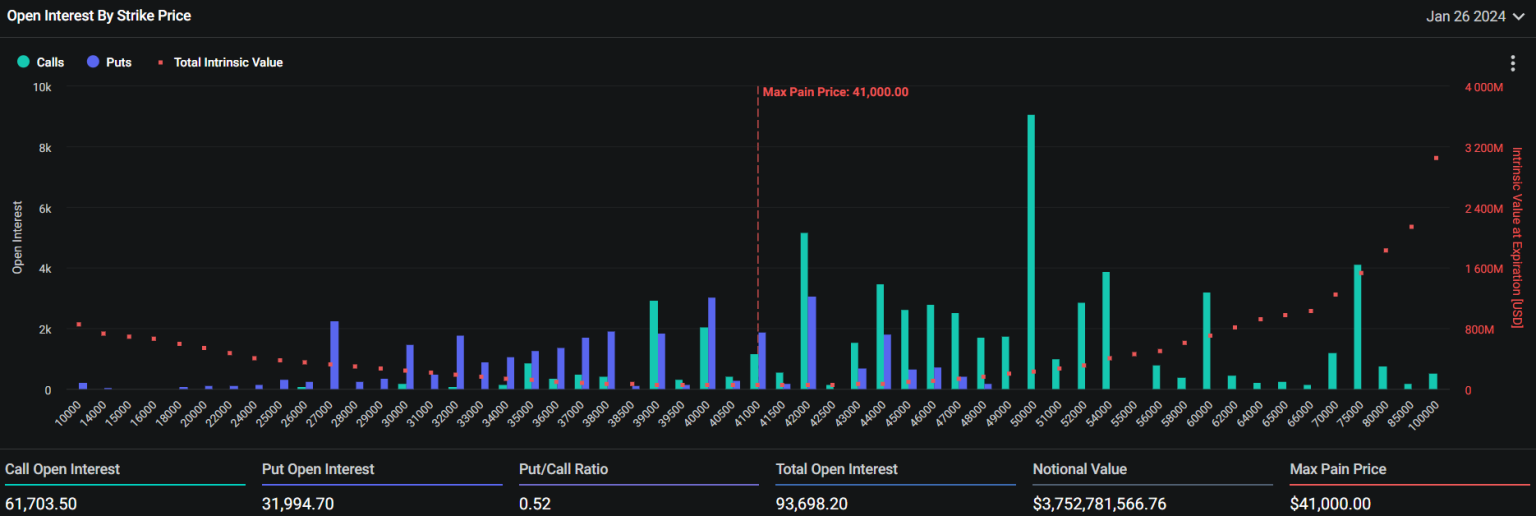

This is a snapshot of the Deribit open interest distribution by strike taken last week before the expiration date and published by Coinpedia. We had an open interest above $350 million in call options struck at the $50,000 level. As the likelihood of reaching this 50,000 level was decreasing, traders would have likely tried to salvage the remaining time value of these call options.

So how does that work exactly?

A trader who buys a naked call option struck at 50,000 on Bitcoin is initially looking to profit from a potential price upside above 50,000. Delta-hedging this option consists of selling some Bitcoin futures, and the amount to sell is the notional of the option, that is $350 million, weighted by the probability for the Bitcoin price to end up above $50,000. As long as this probability is positive, above zero, the option still has ‘time value’.

If the market considers that there is only a 1% probability for the Bitcoin price to reach $50,000, then traders can sell à delta of 3.5 million dollars worth of Bitcoin to try to salvage the time value of the option. Such behaviour would certainly increase market resistance on the upside. As the market goes up, the probability goes up, and the delta size also goes up -> the trader can sell more Bitcoins.

Now given this explanation, we can consider that after the expiration date, the upside resistance decreased. And this would have contributed to the market rebound observed since Friday.

We mentioned in the past that the strikes where we have a very high open interest can act like magnets and help consolidate the market around them. On the other hand, if we are still too far as expiry gets closer, traders will try to salvage the value they can, and theoretically drive the market towards what we call ‘the maximum pain point’. This is where traders salvaged everything they could. Considering the portfolio of all naked options expiring on Friday (no delta), the maximum pain point (here at 41,000) is where the portfolio has its lowest value.

Looking now at the next major expiry this Month scheduled for Feb 23rd, the last Friday of the Month:

We have a high open interest concentration at 50,000: 160 million dollars worth of call contracts. This is currently half the size of the peak observed before the January expiry. The maximum pain point is now at 43,000. The options market is still expecting the Bitcoin price to exceed 50,000 dollars, but as we ll get closer to the 23rd, and there is not much hope in sight, the max pain price would be more likely to realise. The maximum pain point doesn’t hold any long-term information. It is not used to form medium or long-term expectations. It can only be used reasonably to understand better the dynamics near the expiry.

Of course, this analysis offers only one perspective, and market movements are certainly the result of a large combination of many factors, some that are easier to read than others.

Another major factor that has been battering the market up and down is the investment migration from Grayscale’s Bitcoin fund (GBTC) to Bitcoin ETFs. We can see the historical holdings of the fund on this graph produced by Coinglass. The fund sold roughly 127k Bitcoins since the ETFs approval on Jan 10th. That is equivalent to 5.46 billion dollars. It also represents an average of 7,000 Bitcoins per day. Outflows have been slowing down in the past few days. The rebalancing could be performed in a slower and orderly fashion going forward.

Blackrock’s iShares Bitcoin trust now holds more than 2.4 billion dollars worth of Bitcoin: 56,629 Bitcoins as of Monday. Fidelity holds 2.2 billion.

We‘ve had during the week ending Friday, a significant net outflow of 500 million dollars according to Coinshares. The 2.2 billion AUMs lost by the Grayscale Bitcoin Trust have not all been reinvested in other Bitcoin ETFs. Over time, the most competitive ETFs starting with Blackrock’s IBIT will become predominant. ETF investment in general has also been favoured by a new Google policy update in the US, effective two days ago: sponsored ads of US Bitcoin ETFs are now allowed. This should significantly improve adoption.

Tonight, we have the Fed’s interest rate decision followed by the FOMC press conference. The key interest rate should remain stable at 5.5%. We are still in the middle of the earnings season. So far, the number of positive surprises is below average. Most of the S&P500 companies have reported their last quarter earnings. The financial sector is underperforming most.

Regardless, the S&P Index is up 3.84% YTD. The most determinant factor for the market performance this year will be the Fed’s policy. Although unlikely, tonight’s speech will determine whether an interest rate cut can be expected as early as March. But the market is anticipating the impact that these rate cuts would have on growth.

A low-interest rate regime should favour investments in riskier asset classes, including cryptocurrencies.

DISCLAIMER: The information contained herein is not intended as, and shall not be understood or construed as, financial advice. Wirex and any of its respective employees and affiliates do not provide financial, legal, or investment advice. The information contained herein has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for financial, legal, or investment advice. Content not intended for UK customers.