While the meteoric rise in Bitcoin prices takes a much-needed pause, there's good news on the horizon for BTC holders looking for a viable way to hedge exposure. The CBOE Volatility Index (VIX) is progressively becoming the first

inversely-correlated asset (to my knowledge) to provide moderate protection against wildly fluctuating Bitcoin prices. Up until now, Bitcoin remained on an island of its own. As reported by

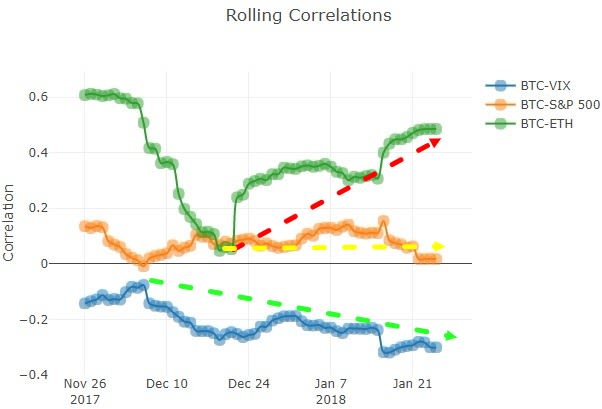

Business Insideron January 21st, Deutsche Bank global financial strategist Masao Muraki is increasingly finding a negative correlation link between the VIX and various cryptocurrencies. This is a potential game-changer for investor adoption, as the dearth of hedging options is relegating many would-be investors to the sidelines. Not only does Muraki observe that the "correlation between Bitcoin and VIX has increased dramatically" in 2018, but he goes on to note "a growing number of institutional investors are watching cryptocurrencies as the frontier of risk-taking to evaluate the sustainability of asset prices". That's powerful stuff. Before we get into how a sustained VIX-BTC inverse asset correlation is a game changer, let's take a look at how this correlation has been developing. Over the past 90-days, the VIX-BTC correlation has seen significant divergence. It has moved from a non-linear relationship (<0.1, Dec. 4-6), to one bordering moderate negative relationship (>0.3, current). The same cannot be said for stocks or crypto's other big brother, Ether, which have flatlined and risen respectively. Take a look.

Even extreme recent U.S. dollar weakness has failed to stem Bitcoin's harrowing drop from $19,000 in mid-December. Despite DXY falling about 6-percent since that time, Bitcoin has continued to plunge lower. This exemplifies how little influence U.S. dollar strength/weakness has exerted on Bitcoin prices to date. Not only is Bitcoin

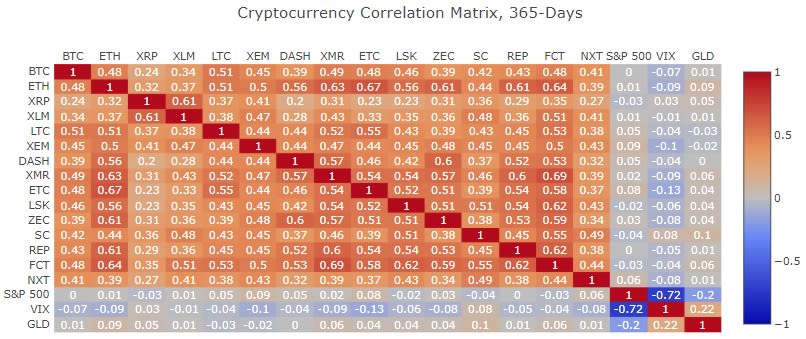

fallingin tandem with the dollar, it's falling about 600% faster over the past 40 days! One simply has to glean a Cryptocurrency Correlation Matrix to understand the incredible challenges facing Bitcoin hedging today. All of Bitcoin's peers are positively-correlated (red), while the S&P 500, gold and VIX have proven ineffective on a 365-day horizon. Again, energy, USD, Yen - all major currencies - no linear inverse relationship has been established. (Source:

Sirf Data)

Correlation among assets is the degree to which they move in tandem. A value of zero denotes no (linear) dependence between the assets. The results can be interpreted as follows:

- 0.5 to 1: Strong positive relationship

- 0.3 to 0.5: Moderate positive relationship

- 0.1 to 0.3: Weak positive relationship

- -0.1 to 0.1: No linear relationship

- -0.1 to -0.3: Weak negative relationship

- -0.3 to -0.5: Moderate negative relationship

- -0.5 to -1.0: Strong negative relationship

Besides the obvious takeaway that no asset has provided a suitable hedge on a 365-day timeline, it is notable how quickly a VIX-BTC inverse relationship has risen over the past 90-days. Rolling correlations have moved from -0.07 (no linear relationship) to over 0.30 today (moderate negative relationship). At these levels, the VIX is providing an

actionable and significantlevel of protection against unhedged BTC exposure. In other words, we're at the point (or almost there) where institutions can develop return distribution models to hedge against bitcoin exposure in a portfolio. This becomes even more relevant now that BTC futures are actively trading on the CBOE.

What This All Means

There are unlimited takeaways one can glean from BTC's developing mirror relationship with VIX. But should trends continue, this relationship will act as a stabilising force on BTC prices going forward. Why? Because emerging hedging options will promote more investors to dip their toe in the water. Instead of staking a directional BTC bet and hoping for the best, investors can offset risk with rises in market volatility. After all, it doesn't matter if you call the market right but get stopped out due to excessive volatility. Adequately hedge through call options or volatility ETFs could be the difference between going broke and restful sleep. If there's one thing Bitcoin desperately needs in order to quell excess volatility, it's wider investor participation. According to

Bloomberg, about 1,000 so-called whales control 40% of the bitcoin in circulation, giving them unrivaled leverage over the broader market. When you also consider that Bitcoin can never float more than 21 million coins in circulation in a world with 7.6 billion people, that's a potential distribution problem. Getting people used to trading in fractions will be a tall order. In the end, the emerging VIX-BTC inverse relationship isn't a call to rush out and buy Bitcoin. Significant regulatory and development challenges remain. There's a reason why China willingly abandoned its multi-billion dollar industry-leading position in BTC, and it portends nothing good for future adoption rates. Remember, China captured over 90% of all Bitcoin trading as recently as December 2016, yet chased everything away. Governments don't abandon dominant leadership positions for flimsy reasons. There's also substantial doubt whether block limit sizes can propel Bitcoin to a mass adoption phase, considering slow transaction times. The more transactions go through, the slower the network becomes. That's not exactly a recipe for success. Regardless, the technology is legitimate and Bitcoin is the undisputed patriarchal leader of its class. For that reason alone, it will have staying power. Whether off-chain Lightening Network technology (in testing) ultimately solves Bitcoin's scalability issue and propels adoption to the next level remains to be seen. But the emerging VIX-BTC nexus has the potential to bring thousands of institutional investors/funds to the party, and that's undoubtedly a bullish development.