We recently announced the launch of X-Accounts, an amazing new way to access DeFi-powered savings on your crypto and traditional currency with none of the fuss or expensive fees!

As well as being super simple to set up in the Wirex app, X-Accounts offer interest rates (IRs) of 6% for ETH or BTC or 12% for EUR and GBP, with an additional 4% if the interest is paid in WXT. The interest is compounded daily and settled on request – so not only do you earn interest on your interest, you can also withdraw your earnings at any time with zero charges.

But how do X-Accounts actually work? Let's break it down.

First things first - X-Accounts are not part of a decentralised framework. As such, all interest payments to X-Accounts investors are covered directly by Wirex. Furthermore, X-Account interest rates - like the best IRs extended to Wirex by third-party decentralised financial platforms - are not set in stone. X-Accounts IRs will be reviewed regularly in line with Wirex’s capacity to source the most secure sources of interest and potentially with our ability to generate profits from core business activities.

We have two main objectives:

- The first one is to outperform X-Accounts’ interest rates.

- The second is to ensure daily liquidity for customers.

In order to reach these objectives in a safe and efficient way, Wirex’s sources of revenues must be both ‘liquid’ and ‘diversified’. There are three main external sources of revenue that we use: DeFi liquidity pools, DeFi lending platforms and institutional lenders.

DeFi Liquidity Pools

Depending on market conditions, the objectives described above might be achieved through decentralised liquidity pools.

A liquidity pool consists of two reserves: one for the ‘base’ token of a pair (e.g. USDC), and the other for the ‘quote’ token (e.g. USDT) of a pair (e.g. USDC/USDT). The pool mid-price of the pair is exactly the ratio of the reserves’ quantities.

A liquidity pool is essentially a market in which a user can swap one token for the other at the pool price: the mid-price adjusted for swap fees and slippage. The process of swapping tokens consists of posting the first tokens in the corresponding reserve and receiving the tokens’ counterpart from the second reserve.

A pool’s creator is effectively providing liquidity on this specific pair. Likewise, a user can provide liquidity to an existing pool by adding tokens in each reserve. The total value of the base tokens added should equal the total value of the quote tokens added. Those providing liquidity as a service would be rewarded with a large portion of the swap fees gathered by the pool.

Coinmarketcap lists the liquidity and estimated Annualized Percentage Yields (APY) accrued to liquidity providers.

Some of the pools Wirex may consider include:

- 1INCH - 1INCH aggregates the liquidity pools of several DeFi projects, including UNISWAP, Sushiswap, or Curve. Its protocol will look for the best execution price among all integrated platforms and pools. The pool’s competitive price attracts more traders, generating greater trading volume and fees.

- UNISWAP - the V3 protocol of the UNISWAP DApp is an automated market maker (AMM) which lets us concentrate liquidity within a price range. In other words, it offers the option to leverage swap fee revenues. If the price were to fall outside the chosen price range, one of the two reserves would effectively deplete, and the liquidity that we had provided would stop earning fees. This would remain the case until the price falls back within the chosen range.

There are hundreds of pools that offer a wide range of returns and rewards (e.g. farming). Rest assured that Wirex is committed to finding the best opportunities for the benefit of our X-Account HODLers.

DeFi Lending Platforms

The derivatives market is also an interesting source of revenue, in which implied interest rates can exceed an annualised return of 20% on BTC or ETH during market rallies. The implied annualised interest rate can be observed through the futures basis spread: the premium of the futures price over the spot price. This spread expands during market rallies, and contracts on severe corrections.

ETH/USD September 21st future over the ETH/USD spot: The market correction typically hurts the future’s premium.

Similarly, high interest rate opportunities that arise in bull markets can also vanish during a strong market correction. Decentralised lending platforms like AAVE or CREAM typically offer Annualised Percentage Yields (APY) between 6% to 8% on stablecoins, but this can reach much more when markets rally. It is also easier to find borrowers during market rallies. This is because they are looking to leverage their positions, and are keen to pay a fixed interest rate to increase their participation if they expect the market to soar by more than 10% within 24 hours.

Institutional Lenders

Wirex has built strong relationships with lenders over the years, including partnerships with leading and vetted institutional digital asset lenders such as Blockchain.com etc. These lenders are vital for sourcing large borrowers of stablecoins and cryptocurrencies.

There is always significant demand for stablecoins or major cryptocurrencies such as Bitcoin or Ether. Financial institutions seeking liquidity for their treasury operations with reduced exposure to cryptocurrency markets can simply tap into the lending market. At the contract’s maturity, they would have to deliver back the currencies they borrow, regardless of their market value.

Lending agreements are legal Over-The-Counter (OTC) agreements, in which an ISDA credit support annex (CSA) defines the terms of agreement relative to the collateral offered, and ensures that losses can be covered.

What are the risks?

The security risk

Regular browser apps or wallets such as Metamask are not adapted for institutional-grade access to DeFi protocols. They would require the user to expose private keys or trust the keeper of a hardware wallet. In this situation, it is hard to centralise or track operations from an accounting or compliance perspective. To mitigate this problem, Wirex has teamed up with Fireblocks, a single, centralised platform used by Wirex to store and transfer cryptocurrencies in and out. A Fireblocks transaction requires multiple secret keys to initiate, which means there is no single point of failure.

Fireblocks have also built a secure network with DeFI platforms like AAVE or Uniswap, letting us interact directly, efficiently and more securely with DeFi pools and loans.

The risk of “impermanent loss”

For DeFi liquidity pools, the risk of having one reserve depleted is the risk of “impermanent loss”. In other words, if we contribute 100% of the pool’s liquidity and traders swap the ‘quote’ token (e.g. USDC) out of the pool, then the pool mid-price will soar. But the liquidity provider (LP) would own more of the depreciating ‘base’ token (e.g. ETH) and none of the soaring tokens.

Undoubtedly, concentrating all the LP’s liquidity in a single pool holds a significant systemic risk. But Wirex has the required levels of liquidity to diversify across several of the most ‘stable’ and most ‘rewarding’ pools.

A stable pool is defined by two highly correlated tokens. Naturally, one of the most stable pools is the USDT/USDC pool that currently rewards the LP with a ~5% annualised interest rate (in current market conditions and without defining a V3 “price range”).

A rewarding pool is one that offers ‘yield farming’: extra incentive rewards for other LPs. A rewarding pool is also intuitively one where both the swap fee level (in % of the traded size), and the ‘trading volume to liquidity’ ratio are high.

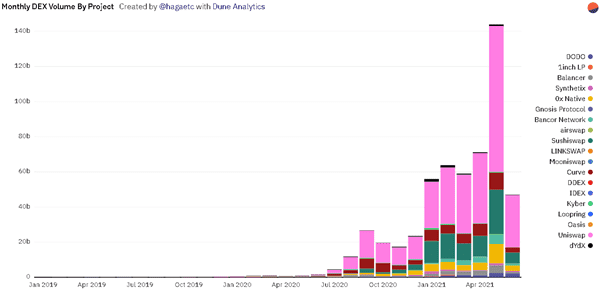

The outlook is very promising in this sector, regardless of the current ongoing market correction. Wirex is counting on the continuous growth of Decentralized Exchange (DEX) volumes to keep or drive pool fees up.

Other risks

Market, Credit, Liquidity and Operational risks are all an inevitable aspect of Wirex’s investment strategy whether trading happens on DeFi venues (Market, Liquidity or Operational) or OTC with institutional counterparts (+ Credit). Our vision is one of a global management of risks and returns in which risks are diversified and opportunities are maximised. In other words, we believe in balancing the highest possible returns against the lowest risk factors.

We rely on trusted third parties to mitigate most of these risks (Credit and Operational), and we strive to mitigate others (Liquidity and Market) through constant monitoring, position rebalancing and a conservative liquidity management approach.

Nonetheless, there is no such thing as zero risk.

X-Accounts

X-Accounts allow us to bring the advantages of DeFi to our retail customers with none of the hassle. As well as seeking to widen access to the benefits of cryptocurrency, we are on a mission to make DeFi secure, affordable and convenient for millions of users around the world.

- X-Accounts represent a safe and easy-to-use alternative to DeFi wallets or browser-based access apps, removing the security headache for Wirex customers.

- DeFi related transaction costs can be significant, especially when transactions occur on the Ethereum blockchain in periods of high market activity (they reached nearly 70$ per on-chain transaction in May 2021). DeFi operations are often complex, involving several transactions: one for the transfer, one for the approval, and one for the actual swap. One operation can easily amount to three times the transaction fee. Guess what? X-Accounts are transaction cost-free.

- Looking for the best DeFi opportunities among the hundreds of pools available can be time-consuming - X-Accounts are convenient, simple and can be set up in a matter of seconds.

- We plan to introduce crypto lending functionality later this year – something that will be an essential part of the X-Accounts feature and enable crypto borrowing capabilities for all Wirex customers. As a result, X-Accounts will have demand from both sides: customers seeking a passive income and those who are looking for crypto loans.