- Discover the vital role of stablecoins in cryptocurrency markets

- Explore their stability, liquidity, and economic impacts

- Learn more here

Stablecoins play a crucial role as safe havens within the cryptocurrency sector, which is one of the most volatile markets. Put simply, stablecoins provide a degree of stability in an exceptionally turbulent environment.*

Furthermore, they presented a compelling alternative to fiat currencies early on, particularly when we compared the ease and cost-effectiveness of crypto transactions (e.g., BTC/USDT) with the more complex and costly crypto-fiat transactions (e.g., BTC/USD). They established themselves as a natural bridge connecting the digital and traditional economies, as well as bridging the gap between blockchains where token transfers might require minutes to finalize, locking up funds in the interim. By utilising stablecoins, users can mitigate market risk and thus safeguard the value of their transfers.

In addition to their safe-haven role, stablecoins serve as a vital reservoir of liquidity for both businesses and individuals. Investors and traders can leverage their long positions to pursue maximum returns on their investments. This leverage mechanism involves depositing a cryptocurrency (e.g., ETH) as collateral to issue stablecoins (e.g., DAI). These borrowed stablecoins can then be used to buy more cryptos (e.g. more ETH), thus increasing market exposure. While leverage can increase market exposure, it may also contribute to heightened volatility in the sector.**

Stablecoins are undeniably foundational in the cryptocurrency sector. Although they lack several key attributes inherent in a Central Bank's fiat currency, they offer the advantage of being independent from centralised entities that could be influenced by political motivations or corruption. This advantage remains limited still by the fiat and cryptocurrencies they rely upon.

Challenges and Limitations of Stablecoins in Cryptocurrency Markets

Stablecoins lack the widespread public confidence enjoyed by the US dollar. This confidence has been eroded by several significant events over the past two years, including the dramatic collapse of the algorithmic stablecoin Terra USD (UST). Before collapsing, UST was the largest decentralised cryptocurrency. It ranked among the top three cryptocurrencies by market capitalisation. Its total market capitalisation exceeded 17 billion dollars. However, this over-engineered stablecoin experienced substantial withdrawals from its liquidity pools on Curve, severely denting the faith of its community. This event triggered a sharp decline in the ecosystem's native cryptocurrency, LUNA, which was designed to support UST's peg.

A stablecoin lacks the level of guarantee that a Central Bank can offer to the public. Its legitimacy is initially derived from its peg to a credible fiat currency.

A stablecoin protocol typically operates in a manner akin to a financial intermediary. For instance, both Tether's USDT and Circle's USDC can be considered as tokenised trusts, ensuring that one US dollar is consistently held and managed by the trust to back each issued USDC. These entities also operate as financial intermediaries because they set a minimum reserve ratio of 1. MakerDAO's DAI, a crypto-backed, over-collateralised, USD-pegged stablecoin, also functions as an intermediary that essentially upholds a high solvency ratio. It applies rules that are comparable to a sound Asset Liability Management (ALM) methodology. Finally, a stablecoin protocol determines borrowing and deposit interest rates much like traditional banks.

Although they operate like financial intermediaries, stablecoin protocols are far from operating like a central bank, and they certainly do not have the luxury of relying on a central bank backstop.

Stablecoins vs. Central Banks in Economic Cycles

Like a central bank, stablecoins argue their capability to generate liquidity as required by the economy, without predefined constraints. For instance, DAI operates on a dynamic supply that could theoretically grow indefinitely. However, in practice, a reserve ratio exceeding 1 restricts the supply of crypto-backed stablecoins, capping it at the value of the cryptocurrencies accepted as collateral. This constraint is effectively illustrated by the Stablecoin Supply Ratio (SSR) reported by Cryptoquant (shown as the blue curve in the graph below): the combined market capitalisation of stablecoins accounts for 7.56% of Bitcoin's total market cap.

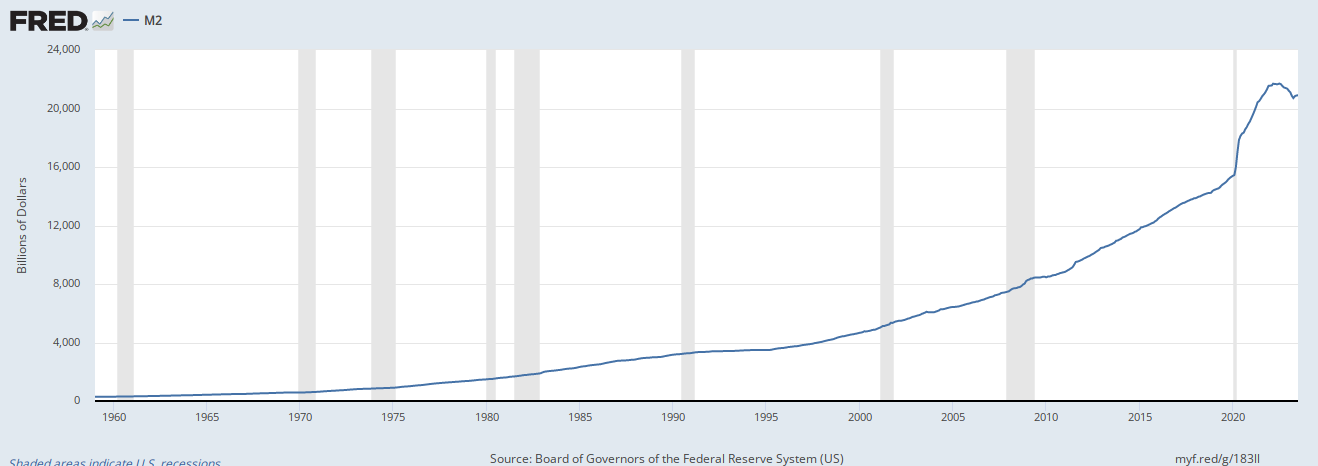

Stablecoins do not serve as a monetary policy instrument within the cryptocurrency market, akin to the role of the US dollar in the fiat market. When examining the USD money supply (M2), it becomes apparent that it has consistently expanded over the years, irrespective of the prevailing economic cycle. Its growth also accelerated during significant crises, such as the subprime mortgage crisis in 2008 and the COVID-19 crisis in 2020, in order to bolster credit lines and avoid bankruptcies.

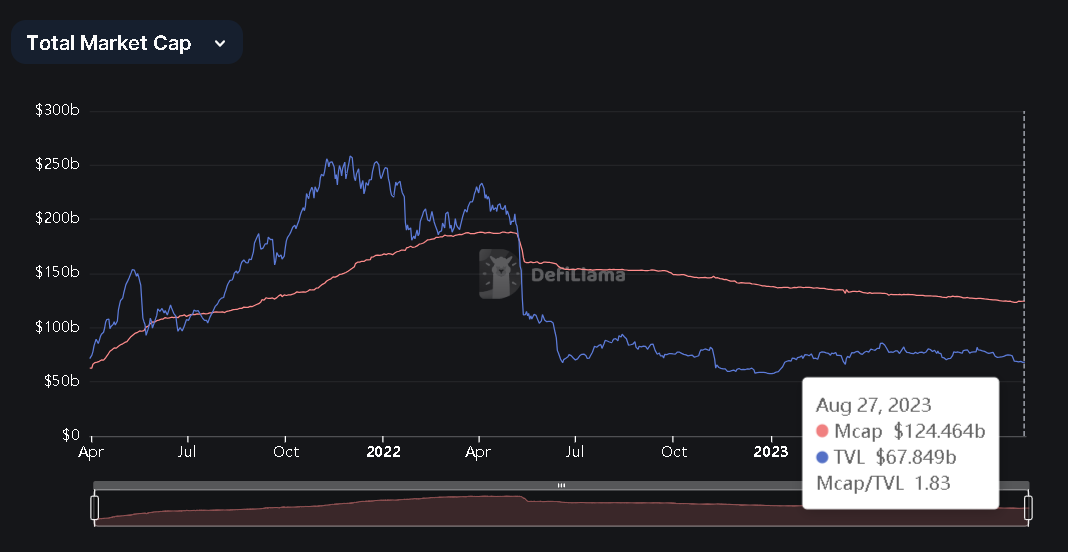

On the contrary, the stablecoin supply tends to decrease during cryptocurrency market crises due to reduced demand for assets within the sector. Funds are exiting the crypto space in favour of safer and more lucrative traditional assets. And the exodus gained momentum following the collapse of Terra's UST stablecoin in May 2022, and after the FTX collapse in November of the same year. These events instilled fear among the surviving hedge funds and market makers, exacerbating the sector's most severe liquidity crisis to date. As illustrated in the graph below from DefiLlama, the market capitalization of stablecoins has declined by 33% since May 2022.

Of course, injecting more liquidity into the cryptocurrency sector isn't economically viable or feasible for a stablecoin protocol. Likewise, providing a liquidity backstop, similar to the Swiss central bank's intervention with Credit Suisse, isn't a possible solution.

The stablecoin supply metric acts as an indicator rather than a tool of monetary policy. It is not looking to cure market crises or control market bubbles. In fact, it is affected by the sector's economic cycles and most likely contributing to inflate market bubbles; In the current context, a declining stablecoin market cap typically signifies a persistent bear market.

In essence, stablecoins favour risk-taking behaviour during bull market regimes and liquidity drought or capital flight during market contractions. They are essential safe havens and practical bridges between digital and traditional economies. Hence, they can also serve as crucial indicators for the sector within economic cycles, measuring its inflows and outflows, reflecting shifts in market sentiment and economic conditions.

* The value of cryptoassets may fluctuate significantly over a short period of time. The volatile and unprecedented fluctuations in price may result in significant losses over a short period of time. Any Cryptoassets may decrease in value or lose all its value due to various factors including discovery of wrongful conduct, market manipulation, change to the nature or properties of the Cryptoasset, governmental or regulatory activity, legislative changes, suspension or cessation of support for a Cryptoasset s or other exchanges or service providers, public opinion, or other factors outside of our control. Technical advancements, as well as broader economic and political factors, may cause the value of Cryptoassets to change significantly over a short period of time.

**The prices of Cryptoassets fluctuate, sometimes dramatically. The price of a Cryptoasset may move up or down, and may become valueless. It is as likely that losses will be incurred rather than profit made as a result of buying and selling Cryptoassets.